Author Cam Hui

Posted: 04 Jun 2013

Surveying the Big Three global economies (US, Europe and China), I see signs of healing – which suggest that markets are likely to continue to grind higher, albeit in a volatile fashion. Let’s take the regions one by one.

US: Muddling through

As I mentioned, I outlined a number of bearish tripwires in my previous post Sell in May?

- Earnings getting revised downwards, or more misses in earnings reports;

- More misses in the high frequency economic releases;

- Major averages to decline below their 50 dma; and

- Failure of cyclical sectors to regain their leadership and defensive sectors to outperform.

With the exception of high frequency economic release data, none of the aforementioned tripwires have been triggered. The chart below shows the decline in the Citigroup Economic Surprise Index, but my own personal impression of high frequency economic data is that the results have been mixed. Even then, bad news may be good news as a weakening economy may provide the impetus for the Federal Reserve to delay any tapering of QE-infinity.

We will have a major test of market psychology this Friday. Supposing that the Non-Farm Payroll misses expectations, will the markets react positively because it is another data point supportive of further QE, or negatively because employment isn’t growing as expected?

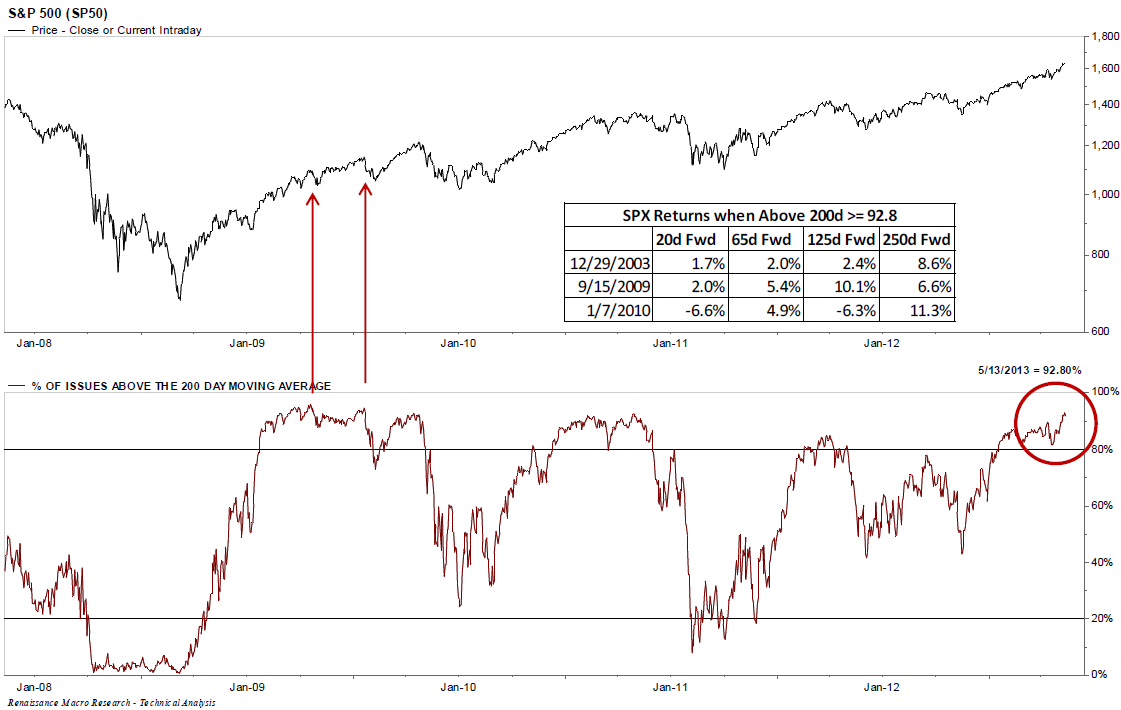

In the meantime, the major market averages remain in a well-defined uptrend. So why are traders so skittish?

In fact, market participants have been so skittish that it only took a minor decline in the major averages for the percentage of bulls from the AAII survey to tank from a crowded long reading (chart via Bespoke). This kind of nervousness do not typically mark major market tops.

In late April, I also wrote that the bearish case also depended on the continued leadership of the defensive sectors and for cyclical sectors to continue to underperform. Well, those trends reversed themselves dramatically in the month of May. The relative performance chart below of Utilities (XLU) and REITs (VNQ) against the market shows that defensive and yield related sectors took a huge hit in the month:

Meanwhile, cyclical sectors as measured by the Morgan Stanley Cyclical Index have started to turn up against the market. What’s more telling is the fact that cyclical sectors performed well in Friday’s market selloff.

Europe: The next step in the Grand Plan

Across the Atlantic, I am seeing signs of healing in Europe (see Europe healing?) What’s more important is the fact that eurozone leaders are taking steps beyond pure austerity measures to address their structural problems.

Recall during the eurozone crises, many analysts said that there were only two solutions to eurozone problems, which was a competitiveness gap between the North and South. Either Greece (or insert the peripheral country of your choice here) leaves the euro and devalues to regain competitiveness, or the North (read: Germany) makes an explicit political decision to subsidize the South. It appears that the latter is happening (from The Guardian) and the focus issue is youth unemployment:

The French, German and Italian governments joined forces to launch initiatives to “rescue an entire generation” who fear they will never find jobs. More than 7.5 million young Europeans aged between 15 and 24 are not in employment, education or training, according to EU data. The rate of youth unemployment is more than double that for adults, and more than half of young people in Greece (59%) and Spain (55%) are unemployed.

Der Spiegel echoed the German “party line” about youth unemployment:

But a new way of thinking has recently taken hold in the German capital. In light of record new unemployment figures among young people, even the intransigent Germans now realize that action is needed. “If we don’t act now, we risk losing an entire generation in Southern Europe,” say people close to Schäuble.

The new solution is now direct country-to-country assistance instead of assistance through the usual EU institutions [emphasis added]:

To come to grips with the problem, Merkel and Schäuble are willing to abandon ironclad tenets of their current bailout philosophy. In the future, they intend to provide direct assistance to select crisis-ridden countries instead of waiting for other countries to join in or for the European Commission to take the lead. To do so, they are even willing to send more money from Germany to the troubled regions and incorporate new guarantees into the federal budget. “We want to show that we’re not just the world’s best savers,” says a Schäuble confidant.

The initial focus of the direct assistance is Spain:

Last Tuesday, Schäuble sent a letter to Economics Minister Philipp Rösler in which he proposed that the coalition partners act together. “I believe that we should also offer bilateral German aid,” he wrote, noting that he hoped that this approach would result in “significant faster-acting support with visible and psychologically effective results within a foreseeable time period.”

Schäuble needs Rösler’s cooperation because the finance and economics ministries are jointly responsible for the government-owned KfW development bank. The Frankfurt-based institution is to play a key role in the German growth concept that experts from both ministries have started drafting for Spain. Spanish companies suffer from the fact that the country’s banks are currently lending at only relatively high interest rates. But since it is owned by the German government, the KfW can borrow money at rates almost as low as the government itself. Under the Berlin plan, the KfW would pass on part of this benefit to the ailing Spanish economy.

This is how the plan is supposed to work: First, the KfW would issue a so-called global loan to its Spanish sister bank, the ICO. These funds would then enable the Spanish development bank to offer lower-interest loans to domestic companies. As a result, Spanish companies would be able to benefit from low interest rates available in Germany.

The concerns over youth unemployment isn’t new. ECB head Mario Draghi spoke about the structural problems relating to youth unemployment in early 2012 (see Mario Draghi reveals the Grand Plan). In a WSJ interview, Draghi discussed what he believed it took to solve the youth unemployment problem [emphasis added]:

WSJ: Which do you think are the most important structural reforms?

Draghi: In Europe first is the product and services markets reform. And the second is the labour market reform which takes different shapes in different countries. In some of them one has to make labour markets more flexible and also fairer than they are today. In these countries there is a dual labour market: highly flexible for the young part of the population where labour contracts are three-month, six-month contracts that may be renewed for years. The same labour market is highly inflexible for the protected part of the population where salaries follow seniority rather than productivity. In a sense labour markets at the present time are unfair in such a setting because they put all the weight of flexibility on the young part of the population.

The first step in the Grand Plan was to gradually go after all the entrenched interests of people with lifetime employment and their gold-plated pension plans, etc. In other words, get rid of the European social model:

WSJ: Do you think Europe will become less of the social model that has defined it?

Draghi: The European social model has already gone when we see the youth unemployment rates prevailing in some countries. These reforms are necessary to increase employment, especially youth employment, and therefore expenditure and consumption.

WSJ: Job for life…

Draghi: You know there was a time when (economist) Rudi Dornbusch used to say that the Europeans are so rich they can afford to pay everybody for not working. That’s gone.

Now that they are taking steps to clean out the deadwood, the next thing to do is to plant, i.e. directly address the youth unemployment problem. These are all positive structural steps and, if properly implemented, result in a new sustainable growth model for Europe.

In the meantime, the Euro STOXX 50 staged an upside breakout in early May and, despite the recent pullback, the breakout is holding:

Stabilization in China

The bear case for China is this: The leadership recognizes that the model of relying on infrastructure spending and exports to fuel growth is unsustainable. It is trying to wean the economy off that growth path and shift it to one fueled by the Chinese consumer. Moreover, it has made it clear that given a choice between growth and financial stability, the government will choose the latter. This was a signal that we shouldn’t expect a knee-jerk response of more stimulus programs should economic growth start to slow down.

Indeed, growth has slowed as a result. The non-consensus call I recently wrote about is that China seems to showing signs of stabilization (see Even China join the bulls’ party). Since that post, further signs of stabilization is also coming from direct and indirect indicators of Chinese growth. First and foremost, China’s PMI came out late Friday and it beat expectations (from Bloomberg):

China’s manufacturing unexpectedly accelerated in May, indicating that a slowdown in economic growth in the first quarter may be stabilizing.

The Purchasing Managers’ Index rose to 50.8 from 50.6 in April, the National Bureau of Statistics and China Federation of Logistics and Purchasing said in Beijing yesterday. That was higher than all estimates in a Bloomberg News survey of 30 analysts and compares with the median projection of 50, which marks the dividing line between expansion and contraction.

Moreover, the KOSPI in nearby South Korea, which exports much capital equipment into China, is behaving well. This is somewhat surprising as South Korea competes directly with Japan and the deflating Japanese Yen is undoubtedly putting considerable pressure on the competitiveness of Korean exports:

Other indirect indicators of Chinese demand such as commodity prices are stabilizaing. Dr. Copper rallied out of a downtrend and appears to be undergoing a period of sideways consolidation.

A similar pattern can be seen in the industrial metal complex:

Oil prices, as measured by Brent (the real global price), is also trying to stabilize:

Key risks

In summary, the overall picture seems to be one of stabilization and recovery around the world. In such an environment, stock prices can continue to move higher in a choppy fashion. There are, however, a number of key risks to my outlook:

- US macro surprise: If we get an ugly NFP this Friday and further signs that US macro picture is slowing, it will negatively affect the earnings outlook and deflate stock prices.

- Japan: John Mauldin has a succinct summary of the issues facing Japan that I won’t repeat but you should read (see Central Bankers gone wild). The issue of a blowup seems to be one of timing and a catastrophic outcome could be close at hand. With bond yields spiking, how will the economy adjust to rising rates? Already, Toyota has pulled a bond issue because of rising rates. Zero Hedge pointed out how JPM has postulated that “a 100bp interest rate shock in the JGB yield curve, would cause a loss of ¥10tr for Japan’s banks”:

The rise in JGB volatility is raising concerns about a volatility-induced selloff similar to the so called “VaR shock” of the summer of 2003. At the time, the 10y JGB yield tripled from 0.5% in June 2003 to 1.6% in September 2003. The 60-day standard deviation of the daily changes in the 10y JGB yield jumped from 2bp per day to more than 7bp per day over the same period.

As documented widely in the literature, the sharp rise in market volatility in the summer of 2003 induced Japanese banks to sell government bonds as the Value-at-Risk exceeded their limits. This volatility induced selloff became self-reinforcing until yields rose to a level that induced buying by VaR insensitive investors.

- An emerging market blowup and subsequent financial contagion: The hints of Fed tapering have negatively affected the emerging market bond market and they are starting to roll over against Treasuries. I am monitoring this chart of emerging market bonds against 7-10 Treasuries carefully for signs of market stress and contagion.

The Short Side of Long has indicated that, in general, sentiment towards equities remain at frothy levels which suggests that a short-term pullback may be in order, However, I am still inclined to stay long equities on an intermediate term basis and give the bulls the benefit of the doubt, but at the same time watching over my shoulder for signs of trouble.

Cam Hui is a portfolio manager at Qwest Investment Fund Management Ltd. (“Qwest”). This article is prepared by Mr. Hui as an outside business activity. As such, Qwest does not review or approve materials presented herein. The opinions and any recommendations expressed in this blog are those of the author and do not reflect the opinions or recommendations of Qwest.

None of the information or opinions expressed in this blog constitutes a solicitation for the purchase or sale of any security or other instrument. Nothing in this article constitutes investment advice and any recommendations that may be contained herein have not been based upon a consideration of the investment objectives, financial situation or particular needs of any specific recipient. Any purchase or sale activity in any securities or other instrument should be based upon your own analysis and conclusions. Past performance is not indicative of future results. Either Qwest or Mr. Hui may hold or control long or short positions in the securities or instruments mentioned.